Bull markets are exciting. Stocks rise, optimism builds, and strong returns can make investing feel easy. But markets rarely announce when the party is about to end. More often, as the saying goes, markets “take the stairs up and the elevator down.”

Today’s environment is a great example. Financial markets have delivered truly impressive growth in recent years, driven largely by the rapid expansion of artificial intelligence. However, alongside that growth, we are beginning to see early signs of excess—developments that have historically appeared later in market cycles.

That doesn’t mean the end is near. But it does mean that discipline, selectivity, and risk awareness matter more than ever.

The last material bear market in US stocks was in 2022 driven by rising inflation, interest rates, and the start of the War in Ukraine. Although stocks technically bottomed in October of 2022, the bull market that has followed can largely be tied back to one event: the launch of Chat GPT to the public on November 30th 2022.

Since then, the market has rotated bullish optimism from industry to industry as the Artificial Intelligence excitement, build-out, and reality has been something the world has never seen.

Within the public markets, the first benefactors were chip companies, particularly those manufacturing GPU’s, or graphics processing units, that run AI “models”, including ChatGPT and Anthropic’s “Claude”. Not too much later, we saw optimism build to the “foundries” that make the chips and the Equipment Manufacturers that create the extremely complex and intricate machinery that the foundries run. At the same time, investors began to ask a question: “Where are these GPU’s going to go?” The answer….data centers – and very large ones at that.

This real estate problem saw demand for a new sector of the markets, physical infrastructure. The topic of my last dividend portfolio letter: Atoms Matter Again | Legacy Group Allen Investments, Data Center Construction saw normally “sleepy” parts of the markets get strong bids from turbines, to utilities, to electrical component manufacturers and more.

As we moved into 2026, we saw this trade evolve. This year, we’ve begun to see companies aggressively raising their prices to take advantage of short supply in some areas, most notably Memory Hardware.

Just 12 months ago, few investors would’ve been able to name the largest providers of this generally “commodity” in the technology supply chain. For decades, these businesses have generally been renowned for being “bad businesses”. A sub-industry of semi-conductors, memory stocks have historically been the most cyclical business line, historically trading at low valuations. These companies have all aggressively pushed pricing to take advantage of the supply/demand imbalance.

Two examples to highlight these changes: First, American company Micron has seen their gross margin, a metric of their “markup” on their products rise from 22.35% in Fiscal Year 2024 to 58.44% so far in 2026 (ThomsonOne). Most dramatically, with two “AI winners”, the Korean Stock Market “KOSPI” index has essentially become a two-stock index. SK Hynix and Samsung have reached nearly 50% of the index through May 2026 (CNBC)

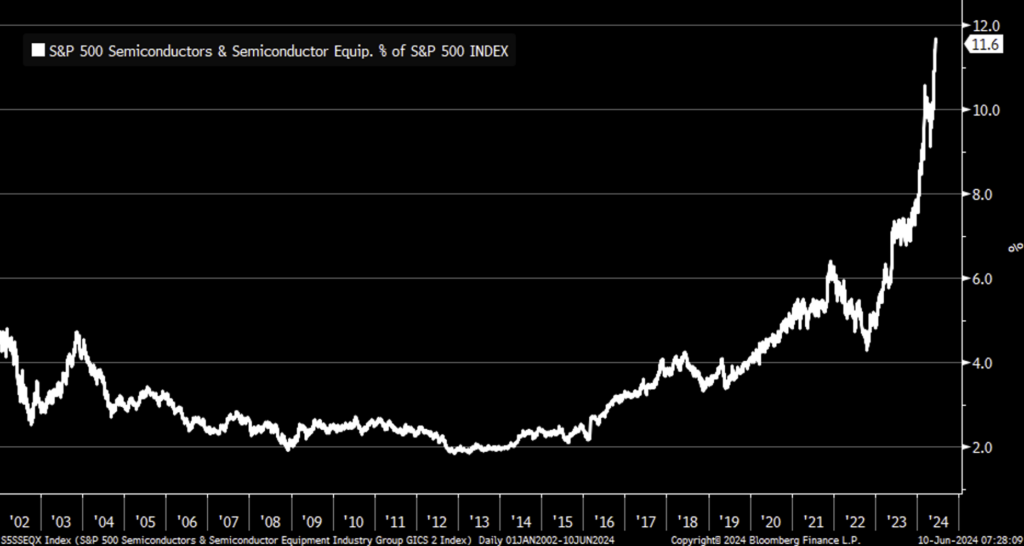

To provide a picture of this growth, I’ve provided below a chart of the rise of Semiconductors as a percentage of S&P 500 market cap over the last 25 years (Bloomberg):

While this data is through 2024, the number has risen to more than 15% by mid-2026. (Morningstar)

If you’ve made it this far, you might be asking a very specific question: Who’s buying this stuff and why is it so important?

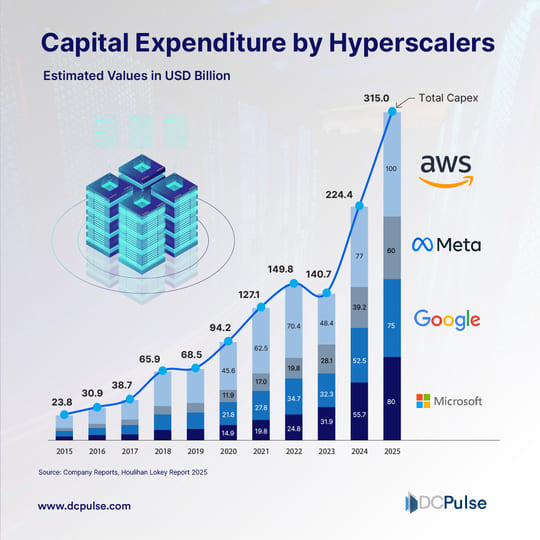

The answer, a collection of companies called “Hyperscalers”. After creating the idea of “cloud computing” in the 2010’s, AI has turbocharged demand for data center solutions. The US Hyperscalers include: Amazon(AWS), Microsoft(Azure), Google(GCP), Facebook, and newcomer Oracle. These companies will have Capital Expenditures in 2026 of over $600 Billion! (theworlddata)

Until 2026, these expenditures have been supported by operating cashflows as these have been historically some of the most profitable businesses the world has ever seen. However, as the scale has grown we have now seen even these companies have to tap debt and equity markets to fund further growth. The below chart, showcasing capex through 2025 for the “Big 4” gives some perspective of this growth:

Part of the difficulty of predicting where things will go from here is the pace of which we gotten here. We’re only about 3 ½ years from when ChatGPT was launched. However, for both the Hyperscalers and the AI Model Providers, this has become a sort of existential race to win. OpenAI, Anthropic, and Google are racing to win the “Model” market and Microsoft, Amazon, Oracle, and new upstart “neo-clouds” are racing to be the primary provider of “compute” to them, and the hyperscalers need a staggeringly large amount of memory to create this compute. What results has been a sort of semi-conductor powered arms race.

While the staggering amount of growth in revenues and stock prices, creates a natural reaction to wonder if the “lights are about to come on”, we encourage everyone to take a step back and look at the earnings that have powered this market.

To that end, profits are rising at unprecedented levels for the 4th year of a bull market. Per LPL Research through 5/26/26, Q1 earnings growth for the S&P 500 was +27.7% with 84% of companies are beating earnings expectations. Revenue Growth was 11.4% year-over-year, and the S&P 500 is projected forward earnings of $346.03 vs. the last 12 months of $289.30 per share. These are truly stunning numbers.

As we look ahead, we may find that just like the oil market over last 10 years, the cure for high prices to be high prices themselves as it encourages new supply to the market.

Also, the cash flow characteristics of the equity markets have changed. After being cash rich and buying back stock for many years, the Hyperscalers are largely now free cash flow negative, with operating cash flow being less than their investments in data center build-out . Growth from here will have real costs in the form of debt that has to be paid back and equity dilution that demands a return on investment. Finally, our investment committee has an eye on what has often been harbinger of last call, rising equity issuance across the markets.

In early June this year, Google announced an $80 Billion stock offering to fund their AI Buildout. (Barrons) Additionally, we’ve completed what’s likely to be 1 of 3 mega IPO’s in SpaceX, OpenAI, and Anthropic slated to likely come public in 2026. These 3 stocks will likely add somewhere between $3 and $6 Trillion of New equity supply to US markets. With a total US Market Cap of roughly $70 Trillion at the start of 2026, this is a material amount of supply for markets to digest (sibliresearch)

Over the past 30 years, there have only been 3 periods where stock issuance has outpaced stock buybacks: The DotCom boom (IPO Frenzy), The Financial Crisis (repairing impaired balance sheets), and 2020-2021(SPAC/Speculative Explosion) (source: Federal Reserve) – All of these periods have been defined by difficult markets afterward, so investors should take caution when evaluating the market ahead.

As we take stock of the markets, we believe that it will continue to be a time that will reward taking measured risks in the markets. While we would caution against the wisdom of rushing in to buy stocks up significant amounts, particularly those with questionable durability to their cashflows, the growth this year has been broad-based across the markets.

It is times like these where we believe it’s vital to remain rooted in a principled approach to investing. As any long-time clients of ours will recognize, we are ardent believers in the attributes of dividend growth investing. While our principles will often miss the highest flyers by virtue of our quality and defensibility screens, there are ample quality businesses also benefiting from the tailwinds of AI that allow investors to see returns.

In application, our approach has been to strike a balance between owning the highest quality AI beneficiaries that we believe will drive high levels of earnings and dividend growth for years to come, while at the same time, diversifying portfolios with companies and industries that are particularly out of favor. While this doesn’t mean running in to double down on companies that may be hurt by AI’s continued development, companies within housing and consumer discretionary stocks more broadly are excellent examples of areas the market has not interest in at the present time. Building these positions today and in the quarters ahead plant the seeds of what we believe will be outperformance in the future.

Finally, we retain the same north star that we always have: the power of dividends. As my partner Keith Albritton has often said “You can eat dividends” – a description of the reality that money is a means to an end, and more specifically a means to meet your lifestyle, legacy, and philanthropic goals, dividends and dividend growth provide a “reality” to stock prices that while exciting on the way up, are often excruciating on the way down. We encourage all investors to keep their goals at the forefront of their investment portfolio and strategies.

Moreover, while we believe this growth is notably different to the late ‘90s, we still don’t know when “the music will stop”. To that end, you may take comfort in knowing that stocks with a “dividend growth” bias have historically outperformed in the after-math of speculative markets. In the early 2000’s, the Russell 2000 Dividend Growth Index outpaced the S&P 500 for 3 consecutive years as the markets struggled to find their footing:

- 2000: +36.2% Russell 2000 Dividend Growth vs. –9.03% S&P 500

- 2001: +5.1% Russell 2000 Dividend Growth vs. –11.85% S&P 500

- 2002: -0.3% Russell 2000 Dividend Growth vs. –21.87% S&P 500

- (FTSERussell & WestmountFundamentals)

While the party is raging and the headliner likely has not even performed, we believe now is the time for patience, discernment, and prudence. Now is a time to remain invested but resist the urge to reach beyond your risk tolerance. We don’t believe markets are poised to exhibit a fall like the aftermath of the Dot-Com Bubble, but we are beginning to see some initial signs of excess that suggest the times of the late 90’s may yet “call” once again. We encourage investors to remain rooted, and focused on their goals, just as we are through our dividend strategies and in everything that we do. It is to that end that we work….

July 2026

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Dividend payments are not guaranteed and may be reduced or eliminated at any time by the company.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

SOURCES – GRAPHS:

SSSEQX Index (S&P 500 Semiconductors & Semiconductor Equipment Industry Group GICS 2 Index) Daily 01JAN2002 – 10JUN2024. Copyright@ 2024 Bloomberg Finance L.P. 10-June-2024 07:28:09.

Source: Company Reports, Houlihan Lokey Report 2025